For many Indian expats and Indian professionals living in Germany, retirement planning can feel confusing and overwhelming. The German pension system is complex, tax-driven and very different from what most people know from India.

Typical questions we hear from Indians in Germany are:

- Should I choose a Base Pension (Basisrente) because of tax savings?

- Is a Private Pension Insurance really better than ETFs or mutual funds?

- What exactly is the Half Income Rule and why does it matter?

This article explains these topics step by step, in simple Indian English, with real-life logic – not marketing promises.

1. Why retirement planning in Germany is different

In Germany, retirement planning is strongly influenced by:

- Income tax rules

- Social security system

- Long-term contract structures

- Limited flexibility in certain pension products

Many Indians focus only on: “How much tax can I save today?”

But the real question should be: “How much money will I actually receive net every month after retirement?”

2. Private Pension vs Basisrente – same numbers, different reality

When you compare offers (for example from Allianz or other insurers), you may see:

- Similar capital values

- Similar projected pensions

- Similar investment performance assumptions

This creates the impression that both products are almost the same. But they are not.

The biggest difference lies in taxation and flexibility.

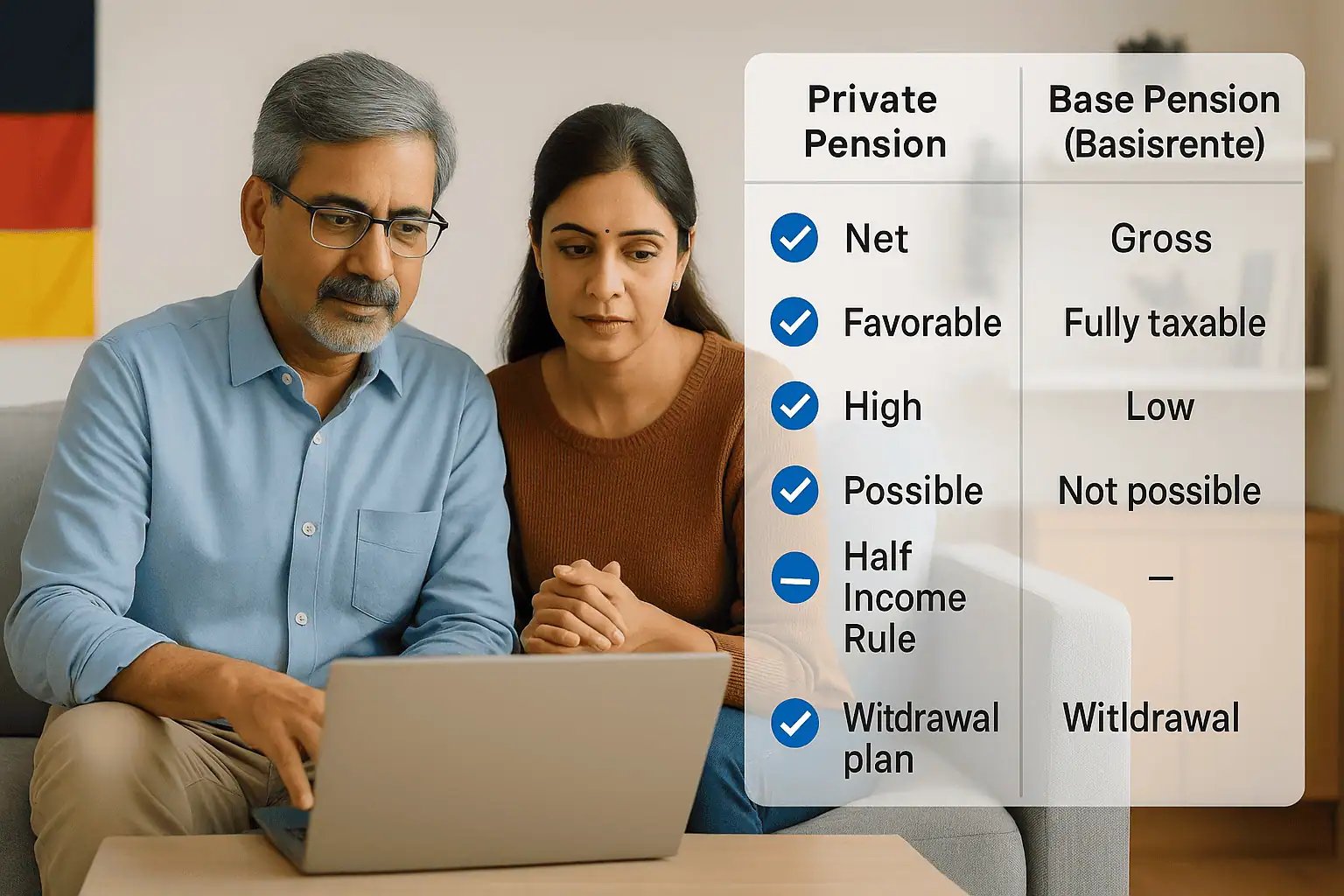

3. Gross vs Net – the most common misunderstanding

Base Pension (Basisrente)

- Pension is shown as gross amount

- Pension income is fully taxable

- No capital payout allowed

- No withdrawal flexibility

Private Pension Insurance

- Pension is often shown as net or tax-optimised

- Special tax rules may apply

- Capital payout possible

- Flexible payout options

Gross income looks good on paper. Net income pays your bills.

4. Example – how taxes reduce real pension income

Let us look at a realistic scenario many Indian professionals face:

| Description | Amount |

|---|---|

| Basisrente monthly pension (gross) | 1,500 € |

| Income tax (approx. 30%) | -450 € |

| Net pension | ≈ 1,000 € |

Depending on your income level, tax bracket and possible future social contributions, 1,500 € gross can easily become around 1,000 € net.

This is why tax savings during accumulation must always be compared with taxation during retirement.

5. Why the Basisrente is very inflexible

The Base Pension (Basisrente) is designed as a strict retirement product:

- No lump sum payout

- No partial withdrawals

- Only lifelong monthly pension

- Strong dependence on pension factor

Once retirement starts, you cannot change the structure. This is a serious limitation for many Indian families.

6. Private Pension – flexibility and planning freedom

Private Pension Insurance offers more control:

- Capital payout option

- Monthly pension option

- Combination of both

- Partial withdrawals

But the biggest advantage comes from taxation.

7. What is the Half Income Rule?

The Half Income Rule is a key German tax advantage for private pension insurance.

It means:

Only 50% of the profit portion is subject to income tax.

This can significantly reduce the effective tax rate in retirement.

8. Conditions for the Half Income Rule (important)

To qualify for the Half Income Rule, both conditions must be fulfilled:

- Minimum contract duration: 12 years

- Payout must start from at least age 62

If these conditions are not met, full taxation may apply. That is why correct structuring from the beginning is essential.

9. Private Pension vs normal investment plans (ETFs)

Many Indians prefer ETFs and mutual funds. These are good investment tools, but:

- Profits are usually fully taxable

- No retirement-specific tax benefits

- No Half Income Rule

Private pension insurance combines:

- Market-based investments

- Retirement tax advantages

- Long-term planning security

10. Withdrawal plans after retirement – a hidden advantage

Some private pension contracts allow a withdrawal plan after retirement.

This means:

- Money remains invested even after retirement

- You withdraw annually instead of fixed pension

- Remaining capital continues to grow

- Half Income Rule still applies

Over 20–30 years, this can make a very large difference in net income.

Frequently Asked Questions (FAQ)

What exactly is the Half Income Rule?

It is a German tax rule where only 50% of the profit part of a private pension payout is taxable, if the contract runs at least 12 years and payout starts from age 62.

Is Basisrente always bad?

No. It can make sense for certain high-income earners. But it must be calculated very carefully.

Is private pension always better?

No. It depends on income, flexibility needs, tax situation and long-term plans.

Can Indians leave Germany and still keep the pension?

In many cases yes, but taxation and payout rules must be reviewed individually.

Why is individual calculation so important?

Two people with the same product can have completely different results due to tax and life situations.

Final thoughts for Indian expats in Germany

Retirement planning in Germany is not about choosing the product with the highest number.

It is about:

- Net income, not gross promises

- Tax efficiency over decades

- Flexibility for life changes

- Correct structuring from the beginning

Understanding these rules is the foundation for a secure and stress-free retirement in Germany.